The humanoid robot market is no longer one broad race between ambitious prototypes. A Humanoid Analytics review of 163 tracked entities shows a sharper split forming between companies with credible customer, deployment, production, or supply chain evidence and companies still trading mostly on funding, demos, shipment claims, or future production targets.

That distinction matters because humanoid robotics is entering a more expensive phase. The sector is moving from videos and prototypes into questions that customers, suppliers, and investors cannot avoid: Can the robots work reliably, can they be manufactured repeatedly, can they be serviced, and will customers reorder after early trials?

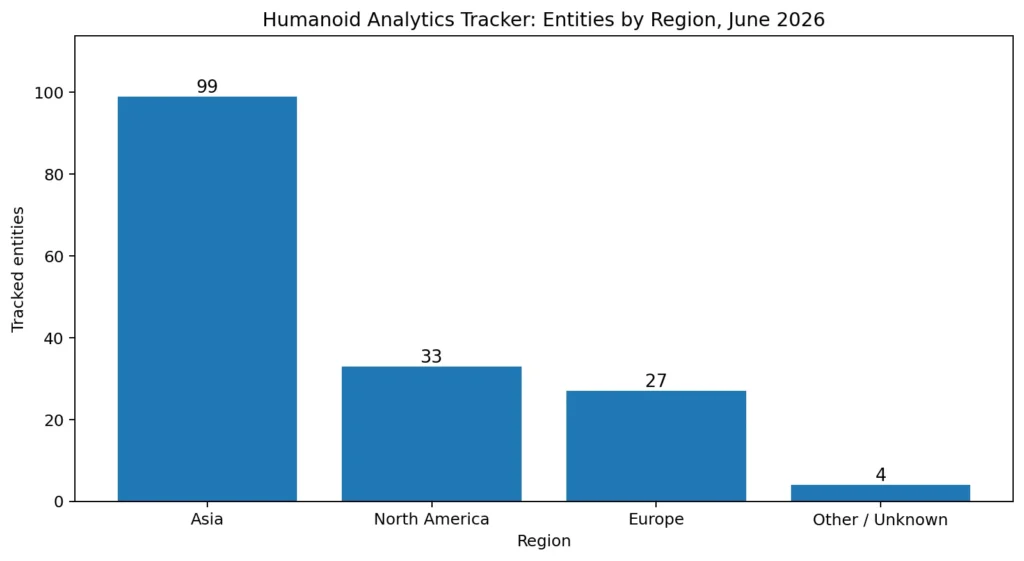

The updated tracker includes 121 core humanoid builders or major corporate programs and 35 dexterous hand or adjacent suppliers. Regionally, Asia accounts for 99 tracked entities, North America for 33, Europe for 27, and other or unknown regions for 4. That geographic distribution is not a measure of commercial success, but it shows where company formation, supplier density, and public humanoid activity are currently most visible.

The chart illustrates the first important market signal: humanoid robotics is not developing evenly. Asia, led heavily by China, has the largest visible company base in the tracker. North America has fewer companies but a high concentration of venture-backed firms and major corporate programs. Europe is smaller by count, but increasingly relevant through industrial customers, suppliers, and manufacturing partnerships.

What the chart does not show is the second and more important signal: evidence quality. A company with a large funding round, a polished demo, or a shipment claim is not necessarily closer to commercial readiness than a company with fewer headlines but a named customer pilot or repeat operational use.

Capital Is Moving Faster Than Deployment Proof

The clearest sign of acceleration is capital. Apptronik said it closed more than $935 million in Series A financing after a $520 million extension round, with investors including Google, Mercedes-Benz, B Capital, John Deere and QIA. Reuters reported the $520 million extension and said the round valued the Austin-based humanoid startup at about $5 billion.

Figure AI is an even stronger example of capital moving ahead of broad public deployment evidence. Reuters reported in September 2025 that Figure raised more than $1 billion in Series C funding at a $39 billion post-money valuation. Figure said the capital would support Helix, its AI platform, and BotQ, its manufacturing effort.

Those rounds are real market signals. They give companies more time to hire, buy components, build production systems, and compete for customers. But funding does not prove that humanoids can perform useful work at a cost and reliability level that customers will accept.

Tesla Optimus shows a different version of the same gap. Tesla describes Optimus as a general-purpose bipedal robot intended for unsafe, repetitive, or boring tasks. Reuters reported in January 2026 that Elon Musk said early Optimus output would start slowly because of the novelty and complexity of the components. That reinforces the tracker’s view that Optimus remains important, but still closer to internal testing and prototype production than public customer deployment evidence.

The Evidence Table Investors Should Watch

| Signal Type | What It Shows | Stronger Evidence | Weaker Evidence |

|---|---|---|---|

| Funding | Ability to hire, build, and survive long development cycles | Large rounds with credible investors and clear use of proceeds | High valuation without deployment proof |

| Customer Activity | Demand from real buyers or operators | Named customer pilots, paid pilots, repeat trials | Generic partnership announcements |

| Deployment | Robots working outside company labs | Operational use in customer environments | Staged demos or event videos |

| Manufacturing | Ability to move beyond prototypes | Production facilities, supplier contracts, delivery schedules | Future production targets only |

| Shipments | Units delivered or sold | Segmented by customer, model, use case, and operating status | Aggregate shipment claims without context |

This table is the core analytical lens for the market. Humanoid robotics is not short of signals. The problem is that many signals are being treated as equivalent when they are not.

A shipment claim is not the same as a deployment. A deployment agreement is not the same as robots already working at scale. A named customer pilot is stronger than a generic partnership, but still weaker than repeat deployment. A production target matters only if it is supported by manufacturing capacity, component supply, quality control, service infrastructure, and real demand.

Deployment Signals Are Scarcer And More Valuable

Companies with named customer activity or credible operating context deserve closer attention. Agility Robotics remains one of the stronger Western examples because Digit has public customer evidence and logistics use cases beyond a lab setting. Agility’s own site describes its humanoid robots as deployed in manufacturing, distribution, and logistics, and the company has announced commercial agreements with customers including Toyota Motor Manufacturing Canada and Mercado Libre.

Agility has also claimed that Digit moved more than 100,000 totes at GXO’s Flowery Branch facility. That is a useful throughput benchmark, although it still leaves open questions about fleet size, uptime, economics, service requirements, and whether customers are expanding deployments at scale.

Humanoid’s agreement with Schaeffler is another important but forward-looking signal. Reuters reported in May 2026 that the UK company plans to deploy between 1,000 and 2,000 robots at Schaeffler manufacturing sites by 2032, with initial deployments scheduled from December 2026 to June 2027 at two German locations. Reuters also reported a five-year actuator supply agreement under which Schaeffler would become a preferred supplier for Humanoid’s wheeled robots.

That is commercially meaningful because it connects a robot developer, an industrial customer, a deployment schedule, and a component supply relationship. But it should still be classified carefully. It is a future deployment agreement, not evidence that thousands of robots are already operating across factories.

China Is Pushing Volume, But Shipments Need Context

The tracker shows Asia as the largest region by company count, and current reporting supports the view that China is becoming the most aggressive humanoid production market. AP reported in June 2026 that Chinese companies are advancing rapidly in humanoid production, while also noting that demand for expensive, still-limited robots can lag production capacity and that real-world use cases are still developing.

AgiBot illustrates both the promise and the caution. The company said, citing Omdia, that it shipped more than 5,100 humanoid robots in 2025 and captured 39 percent of global market share. South China Morning Post reported a similar Omdia-based figure, saying AgiBot shipped 5,168 humanoid robots and led the 2025 ranking.

Those numbers are significant, but they require segmentation. The market needs to know which models shipped, who bought them, whether they were used for research, education, entertainment, inspection, logistics, manufacturing, or customer-facing work, and how many are operating repeatedly in real environments.

1X shows another kind of productization signal. Its official order page lists NEO with a $20,000 ownership option, a $499 monthly subscription, a $200 refundable deposit, and U.S. deliveries starting in 2026. Its product page says NEO is available for preorder and that first orders will ship to consumer homes in 2026.

That is more concrete than a concept video, but it is not yet proof of useful autonomous home robotics. Home deployment raises a different set of unresolved questions around reliability, privacy, remote assistance, safety, support, and customer satisfaction.

The Market Is Growing In Two Directions

The humanoid sector is expanding, but not all expansion has the same meaning. The tracker’s regional data shows a broadening company universe, especially in Asia. The company-level evidence shows something more selective: only a smaller group can point to named customer activity, committed deployment plans, operational benchmarks, or supply agreements that begin to resemble commercial infrastructure.

This is why evidence discipline matters. The industry should not dismiss early companies simply because they lack large deployments. Humanoid robots are technically difficult, and progress often begins in labs, developer programs, controlled pilots, and narrow task trials. But the market should also stop treating demos, capital, and shipment claims as if they prove commercial readiness.

The next useful benchmark is not who has the most compelling video or the largest valuation. It is who can convert pilots into repeat deployments, disclose enough customer evidence to be trusted, manufacture units consistently, and support robots after installation.

Until then, the humanoid market will keep splitting in two directions. On one side is real commercial progress, still early and uneven. On the other is capital-fueled expectation, louder and easier to measure, but not yet enough to prove that humanoid robots are ready for broad adoption.